Clear and stable taxes let to improve investment climate in Republic, also it lead to development of entrepreneurship in Kazakhstan, because now many domestic companies receive, commonly, services from foreign companies in applying new technologies, training of staff, reclamation of new types of services, expanding markets for goods and services.

Conclusion

Since independence the legal system of the country has undergone considerable reforms. The new constitution and a number of new constitutional laws on state system and governmental bodies of Kazakhstan have been passed. Amendments were introduced to the Civil, Criminal and Tax Codes, trade and investment regulations and other legal acts regulating the major aspects of the country life.

Taxes – is basic sources of incomes of the state so the dominant motivation for taxation in any counties is to finance public administration and the public provision of economic and social service. Second motivations are the redistribution of income and correction of market imperfections. But also tax creates distortions in the economy that reduce the real income of taxpayers by more than amount of revenue that is transferred to the government. This occurs when taxpayers either modify their behavior in an attempt to reduce their tax burdens or spend resources in evading taxes. Taxes are used for economic influence of the state on public manufacture, its structure, and on condition of scientific and technical progress. By tax government may discourage domestic production and foreign investments. So government should balanced between public provision of economic and social service, and level of taxation. The appropriate level of taxation depends on a country’s desired role for the state, the efficiency and equity of its public spending, and the efficiency and equity of its tax structure and administration. The Government of Kazakhstan is clearly aware of this and continues to make steady progress in developing its tax system to fit the realities of modern business in the global economy.

Consideration of Nonresident taxation is important because this tax may use as a loophole for avoiding or decreasing tax burden of taxpayers. Level of tax payments is critical to the economic development of Kazakhstan as sovereign state.

So it can decrease level of tax collection and level of social expenditures. Lead to social instability in society.

Appendix A

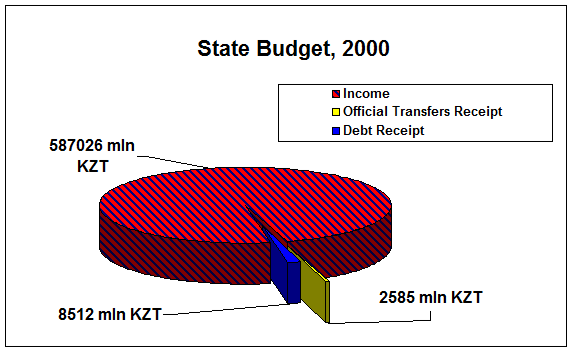

Sources: Statistics Agency of RK, 2001

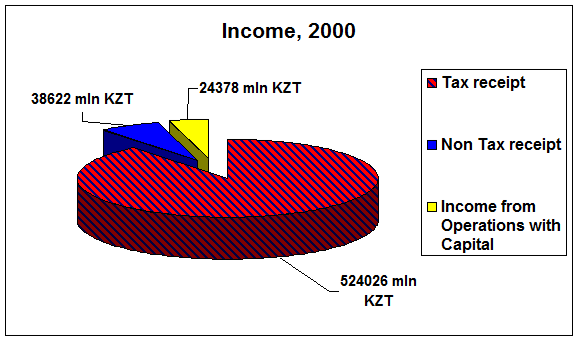

Sources : Statistics Agency of RK, 2001

Appendix B

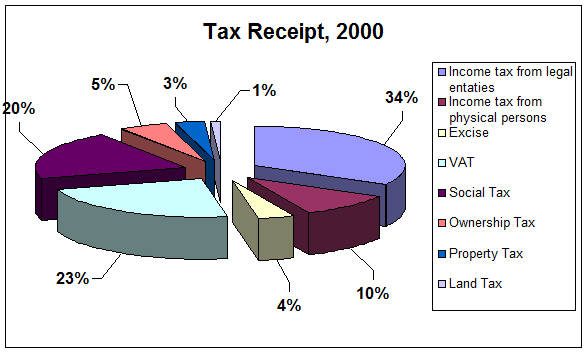

Sources : Statistics Agency of RK, 2001

The tax revenue in the consolidated budget has shown a rising trend in the last two years. The performance of domestic taxes (particularly VAT and Excises) has been improving.

| Income Tax from Legal Entaties | Income Tax from Physical Persons | VAT |

Excises |

Land Tax | Ownership Tax | Social Tax | Property Tax | |

| 1999 | 54759 | 35329 | 89030 | 18956 | 4644 | 24537 | 70463 | 15210 |

| 2000 | 163529 | 51016 | 115132 | 19285 | 5506 | 26693 | 9907 | 14763 |

Sources : Statistics Agency of RK, 2001

THE LIST of USED SOURCES

1. Law of Republic of Kazakhstan from January 1, 2002 " Law on Taxes and other obligatory Payments to the Budget "

2. " Law on Taxes and other obligatory Payments to the Budget " Chapter 7 “Features of Taxation on Nonresidents Income” (with changes from January 1, 2002)

3. Bulletin of Accountant, “Tax Code about Taxation of Operation with Nonresidents of RK " (Print house “BIKO” Almaty, 2001) / 1 – 35/

4. Hodorovich, Mihail Ivanovich 1997, Taxation of Individuals /p25 – 40/

5. Lessons of Tax Reform, World Bank Publication /15 – 25/

6. National Statistics Agency of Republic of Kazakhstan, Short Statistics annual edition of Republic of Kazakhstan (Almaty, 2001) /130 – 135/

7. Kazakhstan Public Expenditure Review, June 27, 2000 (Document of the World Bank)

p /12- 15/

8. Macroeconomics, Timothy Tregarthen 1996 /p328 –340/

29-04-2015, 03:19